I am not a registered investment advisor with the SEC. Nothing in this video, should be taken as legally binding investment advice, in the same way that SEC licensed stockbrokers can advise their clients. I am not “selling” any stocks or OTC penny stocks as a broker in this video. The purpose of chapter 5, is only to offer guidance to those who are interested in educating themselves, about self-directed investing and Biblically Responsible Investing (BRI).

—

Mark 12:17: “Give back to Caesar what is Caesar’s and to God what is God’s.”

UPDATE: 5:32 – 11/2/22 – Correction: if a person gifts you with several thousand dollars, then it is not taxable, so long as it is under $16,000. When you go to file your taxes, you will just fill out a tax-deductible gift tax form (H&R Block and Inspire Advisors agree). The Merrill representative was wrong: gifts are not supposed to be treated like taxable income.

UPDATE: 12:26 – Correction: when it comes to Roth IRA deposits (contributions), you do NOT need to tax that amount a second time. Remember, the Roth consists of “after-tax” dollars. So, if you’re self-employed like me, just always have the habit of setting aside 20% of your income a year into a checking account and then pay the IRS and the state government your estimated taxes through their websites. Anything you have left over, in your “after-tax dollars,” remaining in your savings account: go right ahead and put that into your Roth IRA with a clean conscience. Look at the money in the Roth IRA like you would another savings account. Once you put the money into the Roth IRA, you should have no tax concerns whatsoever (so long as you don’t try to make withdrawals from it before the age of 59).

I am not a registered investment advisor with the SEC. Nothing in this video, should be taken as legally binding investment advice, in the same way that SEC licensed stockbrokers can advise their clients. I am not “selling” any stocks or OTC penny stocks as a broker in this video. The purpose of chapter 5, is only to offer guidance to those who are interested in educating themselves, about self-directed investing and Biblically Responsible Investing (BRI).

—

UPDATE: 12:00 – It is possible that Jesus was a “jack of all trades” when it came to building homes. There seems to be some controversy over whether he was more of a stonemason than a woodworker and vice versa, mainly based on evidence from the church fathers and archaeological findings of houses around Capernaum (see John Schneider, Godly Materialism, p. 201).

UPDATE: 33:22 – John Wesley’s Thoughts on the Present Scarcity of Provisions (1773) and A Serious Address to the People of England, with Regard to the State of the Nation (1778). Wesley was influenced by Rev. Josiah Tucker in this sense. He referred to him as the Dean of Gloucester. A good overview of Tucker’s economic philosophy would be George Shelton’s Dean Tucker and Eighteenth-Century Economic and Political Thought (1981). Along with those whom have analyzed the Great Depression and the 2008 recession, Wesley viewed the depressions of his times to be mainly caused by the housing market. Landlords desired to indulge in expensive living; and raised the rents so high that most people couldn’t handle it; massive unemployment resulted; and prices for all kinds of things inflated to extortionate levels, to make up for the high rents.

UPDATE: 39:45 – Overview of the contents of Michele Cagan’s Investing 101.

At the age of fifty, they must retire from their regular service and work no longer.

–Numbers 8:25–

401(k)s vs. Roth IRAs

Baby Boomers planned for retirement by maxing out their 401(k)s and putting 20% bonds and 75% mutual funds in their 401(k) portfolios. The same trend will probably somewhat exist with Millennials, but I predict there will be more of them using Roth IRAs as retirement accounts and using ETFs instead of mutual funds.

There are two main reasons in favor of choosing a Roth IRA retirement account:

1. Millennials job hop way more than Baby Boomers would have ever thought of. Today’s business culture is now called the “gig” economy. They are (and myself included,) almost completely against the notion of working for one company for 30 years, and planning their whole retirement out, by staying committed to longevity with that one company. Plus employers do not put much stock in their employees anymore, not nearly as much as they used to about 40 to 50 years ago. They often fire people on a whim. The high turnover rates in all these companies make 401(k)s an impractical retirement tool. Sure, people can “rollover” their 401(k)s from one company to another, but this can be difficult at times; and in the best case, it’s a form of financial slavery to the company. It’s a string attached. Also, they often expect you to own stock in your company; and that could lead to an accusation of insider trading in some cases. It keeps people locked down and shackled to that business. Sooner or later, after several job changes and 401(k) rollovers, these people will often break down and finally switch over to a Roth IRA. These allow them to save for retirement, and still be able to change jobs with more freedom, or become independent contractors whenever they’re ready. The bottom line is, that Roth IRAs enable retirement planning along with more employment independence.

2. You pay taxes every year with the Roth IRA in smaller annual amounts. This means that in the long run, you will be able to accumulate more money than you would with a 401(k), because the IRS won’t be able to take out a massive chunk of capital gains tax, from your complete retirement savings of $1 million or more. In 2050, the capital gains tax percentage will also probably be higher than it is now, because 30 years of inflation will have passed. When you’re old, you are going to need every penny of that retirement money, to live comfortably for the last 30 years of your life. Roth IRAers will be able to withdraw all their retirement money when they are 65, without any capital gains tax, except for the tax on that last year’s Roth IRA deposit.

Mutual Funds vs. ETFs: The Battle for Stock Transparency

I can’t explain how or why ETFs have become the new diversified financial product for investors, but they are clearly competing with mutual funds right now. Mutual funds have a longer history that goes back to around the 1920s, but just like Roth IRAs seem to be trending out the 401(k)s, I could see the same thing possibly happening with ETFs trending out mutual funds…in a century or so. Currently the sheer volume of mutual funds held far outweighs ETF holdings, but this might be because of the Baby Boomers. It could be possible that more mutual funds are held by Baby Boomers, but more ETFs are held by Millennials. I don’t know; this would require another study to prove. But exchange-traded funds (ETFs) have been around since the 1990s, and they are built on the same concept: a low-cost stock fund that bundles 100 stocks or more into one investment product, which offers both affordability and diversification, and provides a level of security against the risky fluctuations of the stock market. In the long run, both mutual funds and ETFs, if included within retirement accounts: and if those retirement accounts are maxed out annually: are a practically surefire way to retire with $1 to $2 million, if the deposits are done methodically and repetitively, over a 30 year time span. The key to a good fund selection, is to find one that has a track record of performing better than the S&P 500 on a stock chart. Usually this means that the fund should have at least a 40% return every 5 years. It should look GREEN, and NOT RED, if you were to type the stock ticker into Google and look at its stock chart.

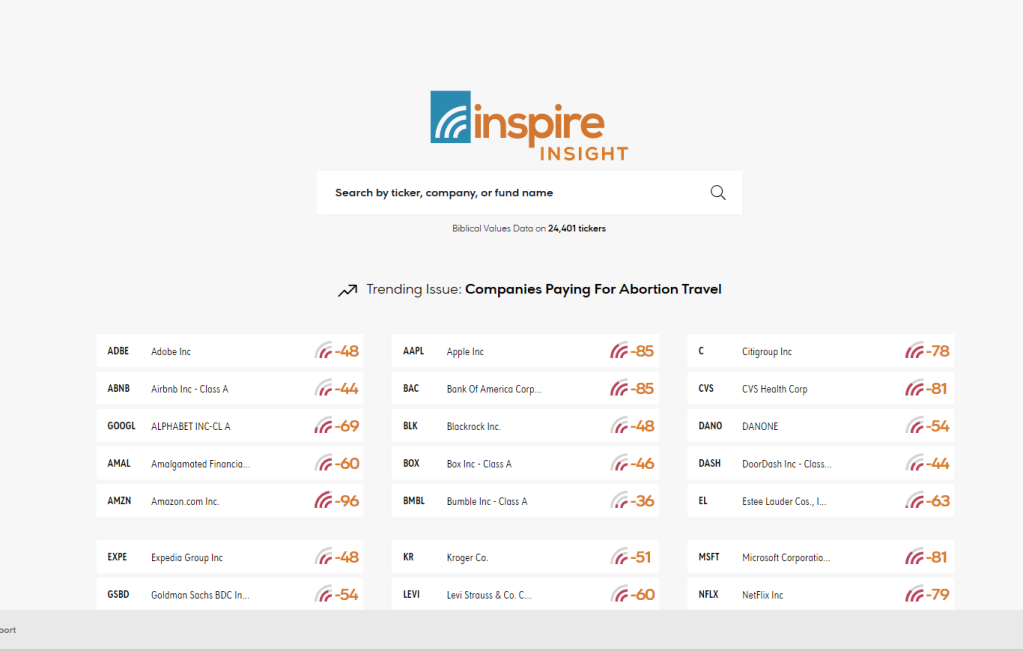

Biblically Responsible Investing and the Inspire Impact Score

My explanation for the rise of ETFs is that it’s probably linked with Socially Responsible Investing (SRI), ESG, green investing, and Biblically Responsible Investing (BRI). Inspire Investing only offers ETFs, for example, at inspireetf.com. Their tickers can be purchased through a Roth IRA account with either Charles Schwab or Fidelity Investments. I personally like BIBL, ISMD, and BLES in terms of their ethical cleanliness and their projected 5 year performance on Google. If they are all invested in together as a trio, then I can’t see why they wouldn’t beat, or at least keep pace with, the S&P 500 when it comes to performance. This BRI firm was founded by Robert Netzly in 2015; and he also published a great book about his BRI philosophy in Biblically Responsible Investing (2018). They probably will never offer mutual funds on principle. Their tool inspireinsight.com shows that they are all about stock ticker transparency. And I will try to say this modestly, but honestly: I think if Timothy Plan, GuideStone Funds, and Stewardship Partners want to keep up with Inspire Investing, then they will either need to use inspireinsight.com on a regular basis, or create other free and publicly available BRI screeners that match or improve on their Inspire Impact Score. If they refuse to do either of these things, then I predict that they will lose more BRI clients to Inspire Investing every year, as more and more BRI investors will become aware of the dirt that exists inside of their BRI funds! They will come to be seen as BRI firms in name only; and probably this is already the case with many Christian investors.

This is a very rare case of Christian business competition, unlike anything I’ve ever run across, in the whole history of Christian economic ethics. Not even the Puritan merchants, competing with each other in London and Boston, have come up to this on a moral level. And I’m sure that they consider themselves all friends, and respect each other professionally and as members of the body of Christ: but in terms of what BRI clients really want: I can tell you what I want: and that is something like inspireinsight.com that will help me make informed decisions about stocks, ETFs, bonds, bond funds, and mutual funds. I would like to see all of the BRI firms make use of the Inspire Impact Score or get out of the BRI business! I’m totally serious about that. I know that might sound impolite, but these are some heavy ethical issues at stake here. And also millions of dollars of misspent Christian money. It should be approached seriously and with a spirit of excellence. I am very sorry to say that these BRI firms have funds that are filled with many stocks that donate to LGBT things, abortion things, hotel pornography, telecom pornography, etc. This has got to break God’s heart! (see 1 Cor. 6:9-11; 2 Chron. 33:6; Matt. 5:28).

Ethical blindness about stocks might have been acceptable in the past, but now Bible-believers just have no excuse. I have even seen Dave Ramsey explain away Biblically Responsible Investing on a recent YouTube video (see “Are My Investments Funding Immoral Companies?”). Do you know why? Because he’s been telling people for years to invest in Timothy Plan. Currently the only Timothy Plan tickers with a positive Inspire Impact Score are the “Israel Common Values” funds (TPAIX, TPCIX, and TICIX). They have a great rate of return that beats the S&P 500, but neither they nor GuideStone Funds will respond to my several emails, that I’ve sent them about all of their Inspire Impact Scores, and all of their very dirty mutual funds! For this reason, I think it’s only a matter of time until the “Israel Common Values” drop into the red on morals. I know this might sound graceless, but maybe it’s time for a little bit of repentance in this area. That way Ramsey won’t have to make excuses for Timothy Plan anymore. If BRI firms want to not only cooperate against worldly investment firms, but also healthily and helpfully “compete” with each other, then they will all have to up the ante on stock transparency with their websites. What a rare case of righteous business competition! I wish more industries had the capability to compete for righteousness’ sake!

The ETF concept and the Inspire Impact Score, are both all about explosive levels of transparency, concerning what is going on ethically inside of all these stock tickers. If that kind of information is not free and publicly available online to BRI investors, then investors will not be able to make informed and clean conscience decisions about their stock investments. It is easier for investors to view the stock holdings inside of ETFs than it is with mutual funds (see Michele Cagan, Investing 101, pp. 109-110). I don’t know why this is, but the ETF websites don’t lie. All of their stock holdings can be seen with the click of a button. ETFs tell me that more and more people care about the companies that they are investing in, due to social awareness and things like environmental, social, and governance (ESG) reports that come out about companies. My guess is that ETF owners generally don’t want to invest for retirement with moral blindfolds on. They are much more willing, to trade one ETF for another throughout the retirement planning process, if they feel like one ETF has fallen off the moral bandwagon. From an ethical investing point of view, ETFs offer more accountability and transparency than mutual funds do. To view the holdings of a mutual fund, you have to dig into their complicated-looking annual reports and their “schedule of investments,” and it is just really complicated to look at. For whatever reason, the way ETFs are created, allows for all of their holdings to be displayed with an out-in-the-open and obvious transparency on their ETF websites.

—

UPDATE: 11/8/22

Mathematically, if you put $2k into BIBL (18% ROI every 5 years), $2k into BLES (10% ROI every 5 years), and $2k into ISMD (16% ROI every 5 years), then they would yield a return of $880 as a trio.

But if you put all $6,000 into TPAIX (45% ROI every 5 years), then the return would be $2,700.

This BRI mutual fund called the Timothy Plan Israel Common Values Class A (TPAIX) matches the performance of Vanguard’s VTI fund and almost matches the S&P 500 (SPX, 48% every 5 years).

If you are a brand new BRI investor and you only have one fund to choose, then I would have to say, that from a performance point of view, TPAIX wins at both having a decent Inspire Impact Score (inspireinsight.com) and an above-average level of performance (Google stock chart).

However, I would also say that if at any point, the TPAIX fund’s Inspire Impact Score goes into the red and starts to accumulate negative ethical violations in the area of LGBT promotion, abortion drugs, and porn, then accept the loss and trade the fund. If such a thing happened, then switch all $6,000 from the fund over to BIBL. Even though the returns would be substantially less (18% every 5 years), BIBL still would qualify for Larry Burkett’s minimum return that a mutual fund should have: 15% every 5 years (Investing for the Future, p. 154). The same goes for ISMD which is performing at 16% ROI every 5 years. Personally for me, I’m going with BIBL as my first fund. It will be easier for me to sleep at night knowing that my fund is getting at least a bare minimum return, but more importantly, it will be in the hands of really, really good ethical screeners. I can’t say that I have the same good conscience and confidence in the screening abilities of Timothy Plan, GuideStone Funds, and Stewardship Partners. They use different screening tools than inspireinsight.com and a subjective “trust me, I got this,” approach, instead of stock transparency and openness. Timothy Plan has been leading the way in BRI since the early 2000s, but unless all of their mutual funds start to acquire decent Inspire Impact Scores, then how could I ever invest in their funds with a completely clean conscience? I don’t want to “trust” a group: I want to see the evidence right in front of my eyes: that such a stock or fund is clean as a whistle. As of the writing, inspireinsight.com is the only tool on the internet that offers this kind of objective and transparent information, that BRI investors need, in order to make informed decisions about their investments. I want to sleep well at night and have that “godliness with contentment which is great gain” (1 Tim. 6:6). I don’t want to worry about my fund slipping into LGBT and abortion promotion overnight! And I don’t mind getting some flak about it: Timothy Plan and GuideStone Funds have awful Inspire Impact Scores. Just awful! How in the world are thoughtful Christians going to be able to put their money into these funds unless they can be assured that they’re clean! Personally if it was me, I’d constantly be in a state of anxiety and worry about such funds giving money to gay pride parades, abortion drugs, and hotel porn, all while they are speaking against such things on their websites. Its inconsistency if their funds are doing this by accident, but hypocrisy if they are doing it on purpose. Jerry Maguire said, “Show me the money!” But I say, “Show me the morals!” Proverbs 16:8 (KJV): “Better is a little with righteousness than great revenues without right.” In either case, open up a self-directed Roth IRA with Charles Schwab to get started. This brokerage house takes both Timothy Plan and Inspire ETFs. You can debate with yourself till you’re blue in the face about whether to go with this BRI fund or that one: all within the safe walls of Charles Schwab.

I’ve noticed that this subject of houses is very controversial among Christians. This becomes one of the primary things that people drill into when they are trying to judge a prosperity preacher on TBN and label him a false prophet. I would advise using charity and mercy towards people in your church, family, circle on this very controversial and very divisive subject. This falls within the purview of PERSONAL finance for a reason. I don’t believe it is polite, charitable, or gracious to be stirring up conflict with other believers over house size, etc, (Rom. 14), but when it comes to a person’s personal sanctification, it might be a thing to be considered: living a Spartan lifestyle over and against a luxurious one. I lean toward simplicity because the Bible says to associate with the lowly (Rom. 12:16); and that its too easy to forget where you came from, and have your heart lifted up with pride, if you are not intentional about avoiding luxury homes or items. Living in a modest home also has a leveling effect on social relations. Too many people’s careers are simply not “competitive” enough to attain an upper middle class or luxury home (2% of Americans are upper class; and 25% are upper middle class; that is, about 75% of Americans live in “modest” living conditions); and so if a person can “afford” to live in a luxury home and then decides to do so, that can create a sense of one-upmanship, tacitly or openly. The homeowner will probably be viewed by others as materialistic, even if they are not. The homeowner might also be frequently tempted to view others in modest living conditions to be living a “substandard” lifestyle, and develop a snobby attitude. In a fallen world racked by temptation, sin, and trials, it seems that owning really nice houses has a tendency to create obvious social divisions that make it impossible for most people to compete with, or to be understood. Mind you, its not the paycheck amounts that is the socially dividing issue as much as the purchase of luxury homes and other like things: because these things come into view at social events. See also my video on “Biblical Economics 144: Is It a Sin to Live in a Nice House?” –J. B., 4/9/24

11 Be careful that you do not forget the Lord your God, failing to observe his commands, his laws and his decrees that I am giving you this day. 12 Otherwise, when you eat and are satisfied, when you build fine houses and settle down, 13 and when your herds and flocks grow large and your silver and gold increase and all you have is multiplied, 14 then your heart will become proud and you will forget the Lord your God, who brought you out of Egypt, out of the land of slavery. 15 He led you through the vast and dreadful wilderness, that thirsty and waterless land, with its venomous snakes and scorpions. He brought you water out of hard rock. 16 He gave you manna to eat in the wilderness, something your ancestors had never known, to humble and test you so that in the end it might go well with you. 17 You may say to yourself, “My power and the strength of my hands have produced this wealth for me.” 18 But remember the Lord your God, for it is he who gives you the ability to produce wealth, and so confirms his covenant, which he swore to your ancestors, as it is today. 19 If you ever forget the Lord your God and follow other gods and worship and bow down to them, I testify against you today that you will surely be destroyed. 20 Like the nations the Lord destroyed before you, so you will be destroyed for not obeying the Lord your God. –Deuteronomy 8:11-20

Jesus began to speak to the crowd about John: “What did you go out into the wilderness to see? A reed swayed by the wind? 8 If not, what did you go out to see? A man dressed in fine clothes? No, those who wear fine clothes are in kings’ palaces. 9 Then what did you go out to see? A prophet? Yes, I tell you, and more than a prophet.” –Matthew 11:7-10

One person pretends to be rich, yet has nothing; another pretends to be poor, yet has great wealth. –Proverbs 13:7

Why is self-denial in general so little practised at present among the Methodists?…The Methodists grow more and more self-indulgent, because they grow rich…And it is an observation which admits of few exceptions, that nine in ten of these decreased in grace, in the same proportion as they increased in wealth. Indeed, according to the natural tendency of riches, we cannot expect it to be otherwise. But how astonishing a thing is this! How can we understand it? Does it not seem (and yet this cannot be) that Christianity, true scriptural Christianity, has a tendency, in process of time, to undermine and destroy itself? For wherever true Christianity spreads, it must cause diligence and frugality, which, in the natural course of things, must beget riches. And riches naturally beget pride, love of the world, and every temper that is destructive of Christianity. Now, if there be no way to prevent this, Christianity is inconsistent with itself, and, of consequence, cannot stand, cannot continue long among any people; since, wherever it generally prevails, it saps its own foundation. But is there no way to prevent this? To continue Christianity among a people? Allowing that diligence and frugality must produce riches, is there no means to hinder riches from destroying the religion of those that possess them? I can see only one possible way; find out another who can. Do you gain all you can, and save all you can? Then you must, in the nature of things, grow rich. Then if you have any desire to escape the damnation of hell, give all you can; otherwise I can have no more hope of your salvation, than of that of Judas Iscariot. –John Wesley, “Causes of the Inefficacy of Christianity” 1.16-18

—

The size of the “fine houses” in Deuteronomy 8:11-12 is not specified, but reason seems to suggest that a house should be proportionate to the size of the family. It seems that when people begin to covet after half-million and million dollar luxury homes—when they have only two or three children, or none—that earthly-mindedness has set in. Such a posh display of materialism is hardly Christian. In the past, men of God purchased homes that correlated to how many children they had in their families. Archaeologists in the Catholic Church, believe that they have discovered St. Peter’s House in Capernaum, the remains of which are about 100 square feet (see Douglas Kennard, Petrine Studies, p. 59). This is not to say that this was the total size of his house. Capernaum was the same town that Jesus lived in as a single man (Matt. 4:13). Other archaeological digs in the nearby town of Chorazin, uncovered nearly perfect samples of houses, with several built around the size of about 900 square feet (or 30 feet x 30 feet). “They are square-built—sometimes thirty feet square—with one or two columns down the centre to support the flat roof, which in all Eastern countries is an important feature of a house; the walls are two feet thick, built of masonry or blocks of basalt, with low windows twelve inches high by six inches and a half wide, and each house is divided into four chambers. Simon Peter’s house may have been, and probably was, after this stamp” (see Edwin Hodder, Simon Peter: His Life, Times, and Friends, p. 77).

These Biblical homes of the lower and middle classes are comparable to how the Ingalls family lived in Little House on the Prairie. We’re talking about small cottage-sized homes. Really small houses by most people’s standards today. They are almost like Jed Clampett’s old cabin that everyone laughed at in the first episode of The Beverly Hillbillies. John Bunyan’s house, which was a pilgrimage site for quite some time, was called “Bunyan’s Cottage.” Richard Baxter and John Wesley lived in small houses. The house where the Pentecostal Movement began, was a cottage that barely exceeded 1900 square feet, with four bedrooms and two bathrooms (216 N. Bonnie Brae St., Los Angeles, CA). Pentecostals used to call their house church gatherings “cottage prayer meetings,” because having a small, modest house was acceptable by holiness families at that time. Leonard Ravenhill, the holiness preacher, lived in a ranch-styled home slightly larger than a cottage in Garden Valley, Texas. This was given to him as a gift from David Wilkerson (see Mack Tomlinson, In Light of Eternity: The Life of Leonard Ravenhill, p. 459). The only saints that I’m aware of, who had large houses were Martin Luther, Daniel Defoe, and Charles Finney (the “Finney House”), but they all had around six to seven children.

The house that St. Francis of Assisi grew up in, might not be as physically impressive as you would think, at the first glance. But after centuries of wear and tear, it remains intact in Assisi, Italy. It’s made of carved stones and windows and has a very fortified look to it. Other parts of the house have fine stonework on the walls and ground; it’s a fine work of stonemasonry, with a fine set of stone stairs. I’m sure this would have qualified as a luxury home in the medieval times. It’s not a castle by any means, but it was at least an upper middle class house, and might be closer to what Moses meant by a “fine house” in Deuteronomy 8:12. In any case, this was the style of house that St. Francis walked away from; but more than that, he rejected the anti-spiritual views of business, personal finance, and materialism that were adopted by his father. The spiritual rewards of this sacrifice that he made, led to a life that was absolutely filled, with paranormal manifestations of God’s Spirit (see “The Life of St. Francis,” Bonaventure, Paulist Press, 1978).

The U.S. government seems to agree with the saints that small houses are better for people. Look at the single family homes that they sell through the USDA and HUD. Nothing usually exceeds $100,000. They are modest and proportionately sized. It would be natural for some very large families, with eight to ten kids, to aim for a house around $500k if it had around five bedrooms or more. The kids could share rooms with bunkbeds. But for a rich or retired couple, without children, to desire to live in a $500k or million-dollar home of any amount, is beyond reason and not a conservative use of living space. And it’s too much to clean! Someone in this situation probably considers luxury to be more important than faith and relationships.

It’s no wonder to me, that such mansions can end up haunted, like in the old 1963 movie The Haunting (Rev. 18:2). Then there’s the Haunted Mansion ride at Disney World: which speaks to me of something assumed in the fears of American culture. Haunted houses are a thing that some real estate agents have to deal with! But they will keep it hush-hush and joke about it. There are articles written quite seriously about this if you look for them. I’ve seen one or two on realtor.com. Interesting to look at the common traits they share. They are often old, haunted luxury homes, but not always. The classic horror trope is a gothic-looking haunted mansion from the Victorian era: the Edgar Allan Poe, Vincent Price, and Addams Family sort of image. Such houses are viewed as “cursed” by the demonic as a punishment on the owners for some grave sin against the ten commandments, such as murder or witchcraft (Exod. 20:3-17). These houses are so filled with poltergeist activity that nobody ever wants to live there; and so they become uninhabited by man, and will fall into disrepair. The very nature of a luxury home assumes that the command of “thou shalt not covet,” was being ignored by the previous owners as well. The Catholic Church has a series of prayers for the blessing of such a demon-possessed house in the Roman Ritual. They can be found, and used if necessary, with “The Exorcism of Haunted Houses,” in Herbert Thurston’s Ghosts and Poltergeists (1953). The TV show Unsolved Mysteries released a DVD collection on ghosts (2004). If you watch that, then you will see what I mean. Hauntings don’t always happen in large mansions and luxury homes, but they often do.

This video is posted with permission from Compass International.

32:00 – I disagree with his pro-luxury home comment he makes here. Scripture has very negative things to say about luxury of all types; and “fine houses” are included (see Deut. 8:10-14; Ezek. 26:12; Prov. 13:7; 30:8; Heb. 13:5; James 5:5; Luke 16:19; 1 Timothy 6:17-18; Matthew 4:13, 12:42, and Mark 6:3).

I am not a registered investment advisor with the SEC. Nothing in this video, should be taken as legally binding investment advice, in the same way that SEC licensed stockbrokers can advise their clients. I am not “selling” any stocks or OTC penny stocks as a broker in this video. The purpose of chapter 5, is only to offer guidance to those who are interested in educating themselves, about self-directed investing and Biblically Responsible Investing (BRI).

—

UPDATE: 10/23/22 – Treasury bonds that mature in 30 years are the best thing to put into your IRA for retirement. The 5% annual growth will be long-term and you won’t have to think about selling them until you’re in your 60s. Not treasury bills, as most of these are short-term and mature their interest growth in just a few years, same thing with treasury notes. In Larry Burkett’s time, in the 1990s, treasury bills were really expensive. Now treasury bonds, bills, and notes can all be bought through Merrill Edge or Fidelity for $100 a piece (see Michele Cagan, Investing 101, p. 68).

Fidelity Investments (established in 1946, and originally Peter Lynch’s employer, coincidental last name, and of no relation to the co-founder of Merrill Lynch,) is the main online broker of a Roth IRA that accepts Timothy Plan’s mutual funds and Inspire Investing’s ETFs. TD Ameritrade also takes them, but they’ve only been around since 1975, are financially weaker, and have suffered security breaches.

THE SELF-DIRECTED ROTH IRA INVESTMENT PORTFOLIO: Roth IRAs should consist of 20% treasury bonds that mature in 30 years and 75% BRI mutual funds, such as the Timothy Plan “Israel Common Values” mutual funds (TPAIX, TPCIX, TICIX) and high-return or “blue chip” individual oil stocks and other industry growth stocks (AMR, OXY, DVN, CF, VLO, EOG). 5% should remain in your Roth IRA as unspent cash (see Don Underwood and Paul Brown, Grow Rich Slowly: The Merrill Lynch Guide to Retirement Planning, p. 257). Individual stocks can be screened for low P/E ratio, price, market cap, industry, sector, etc, on finviz.com. Enter any stock ticker into Google and it will show you the stock chart along with the expected 1-year and 5-year returns. I’d say, don’t purchase anything that won’t give you at least a 40% return in 5 years (unless it’s treasury bonds). A 40% return every 5 years is considered normal for the top performing secularly managed mutual funds (for example: VSMPX, VFIAX, FXAIX). These are not BRI funds, but they are what the world would consider to be normal, healthy performing examples of mutual funds. All mutual funds and stocks should be plugged into inspireinsight.com to confirm that they are ethically “clean” according to BRI and ESG standards.

—

OLD-TIME INVESTMENTS SINCE THE 1600s

Gold Coins (2% to 5%):moneymetals.com, apmex.com. (Canadian Maple Leaf AND/OR cash in the Roth IRA; Fidelity allows you to buy these as well).

I am not a registered investment advisor with the SEC. Nothing in this video, should be taken as legally binding investment advice, in the same way that SEC licensed stockbrokers can advise their clients. I am not “selling” any stocks or OTC penny stocks as a broker in this video. The purpose of chapter 5, is only to offer guidance to those who are interested in educating themselves, about self-directed investing and Biblically Responsible Investing (BRI).

Beware of false prophets, who come to you in sheep’s clothing but inwardly are ravenous wolves. –Matt. 7:15

Young men, all of you, beware of false guidance from men who may have ulterior motives to control you for various purposes. They may be dads, uncles, or grandpas, or even pastors. I had a pastor once when I was in high school and he said, “You’re called to the ministry.” That altered the course of my life mission and my educational pursuits at college. And I believed him. I believed every word of what he said, because I had a passion in my heart to feel and understand and know the witness of the Holy Spirit. And I was very much passionate about charismatic worship every Sunday: truly, and really feeling God’s presence all around me, dancing like David (2 Sam. 6). But I didn’t realize, that in my youthful ignorance, I don’t think very many other people were genuinely feeling the presence of God in that church. I think that I was experiencing what they call prevenient or saving grace at that stage, but I am now not so sure if there was anyone else feeling God’s presence. It wasn’t ever talked about by others. Perhaps I was being “elected” by the Holy Spirit, who knows.

In any case, I was not called to the ministry, at least in that pastor’s church. Sooner or later, the time came where I spoke to the pastor and his son (my best friend,) at Starbucks one night. I reminded him that he said I was “called to the ministry,” and I let him know I was interested in studying theology and going to college for it. He looked me square in the eye, and then he says, “I’m never giving you my pulpit.” In a really cocky tone of voice. I was really surprised at him with this. I didn’t quite understand what his motives were originally: why he told me the year or so before that I was called to the ministry; and now he says that he’s never going to give me an opportunity to preach a sermon, to share the things that were stirring in my heart. I had read the Bible back to back by then and was really on fire for God: I wanted to share the Gospel with the lost. And I did sometimes go with his son to do that at the local state university. I don’t quite understand why this pastor pulled this about face. No explanation was given; and it was very confusing, frustrating, and disappointing. Maybe he thought that because I was just a simple teenager, that I was too young to say anything of spiritual value. Maybe he thought I hadn’t “proved faithful” to the church for 20 years straight so he could finally “release” me to preach sermons. God knows what was going on in his head, because he sure didn’t let me know anything further.

Another thing that really baffled me is that my best friend, who was present there, just kind of went along with everything he said; and never really expressed any disagreement with anything that his dad said. And I understood that I was transparent about my temptations and sins with him; and maybe that had something to do with it. But in any case, that’s no way to handle a young man who you genuinely believe is called to a preaching ministry. That young person should be guided, and coached on how to overcome temptation, or whatever other hang-ups he had about me, not being allowed to preach in his church. Since that day, as far as I know, this pastor has barely ever given the opportunity for any of his three sons to preach anything from their experiences. My best friend in fact went on for about 15 years in foreign missions in various South American countries, sacrificing his comfort over here in America, hoping that the time would come when he would finally be able to preach about the Gospel and Pentecostal experience, and do good works for Christ (Eph. 2:8-10). But because he had been so transparent about his temptations, shortcomings, and sins with the pastors down there: they did not give him any opportunities to preach anything; and basically relegated him to the status of an altar boy for years. That is not spiritual leadership. That’s taking advantage of a young man’s trust! I really truly wonder how many times pastors lie to young men, every year, by dropping the line “you’re called to the ministry,” but they have absolutely no desire to let them ever say anything to anyone during a church service. It is through our lives that we worship God, but it is through the “ministry of the Word” that we create impact on others for Jesus (Acts 6:4). It seems to me, that by and large, saying “you’re called to the ministry” is a deceptive little lie that reckless pastors often say, just to motivate otherwise unmotivated young men, to keep on attending their church services.

I don’t quite understand how pastors can manipulate young men like this; and claim to have a clean conscience: promising them opportunities to do good works for Christ: and then afterwards, not give them opportunities to do good works for Christ. What is supposed to be accomplished by that? Why lead them on? Why tell them that, “Yes, you’re called to preach,” and then turn around and give them toilet cleaning duties, and never give them any opportunity to preach? Or have any spiritually developing coaching sessions with them. Or give them a concrete step-by-step ministry training program that they can go through and finally end up preaching something valuable? How many would-be soldiers in the army of God have been aborted by this deceptive and sinful practice, due to discouragement alone? My only explanation for this sort of behavior is that it’s nothing but manipulation on the pastor’s part. He’s only telling this to certain young men to make them ambitious and egocentric, and to feel important, so that they will keep on attending the church services, and fill up the seats to make his church look good on a superficial level. There is nothing, no genuine desire for spiritual mentoring going on there at all. What’s worse, and in the case of this particular church, is now what was once the most rebellious (however good-looking,) daughter of this pastor, is speaking almost every other Sunday there; and none of his three sons ever are. Why is this? Maybe its a marketing spirit at work. Using pretty girls for advertising is one of the oldest business tricks in the book of sales. Sermons should be preached by the men with the highest level of devotion to God. Not because you’re pretty. Not because you make a lot of money. Devotion to God! Consecration, and not carnal reasoning, is what we need in our pulpits! Oh that God would raise up another Wesley to train an army of open air preachers!